Research & Development

What is an R&D Tax Credit?

The Research & Development (R&D) tax credit is a credit that is available for the

development or improvement of products, processes, techniques, formulas, inventions or software. It

is intended for companies who undertake R&D that is directly related to their industry to claim an

extra deduction for certain qualified expenditures in which the claim amount is dependant on which

credit scheme your company uses.

Direct and externally provided staff, subcontracted R&D,

software directly used, trials, consumable items, prototyping and collaborative work costs may all

qualify for an R&D credit. Capital expenditures, the cost of land, the cost associated with the

creation of patents or trademarks or the cost associated with the production and distribution of

goods and services does not qualify under the schemes.

A company can claim for the salaries,

wages, class 1 National Insurance Class (NIC) and pension fund contributions for staff directly and

actively engaged in the ‘hands on’ R&D project. Additionally, a proportion of supervisory and

managerial time spent specifically directing such employees in those activities could be claimed as

well.

R&D Tax History

The amount of spending done by the United Kingdom on R&D has fallen behind what is being spent by

many other countries. To build a modern knowledge base, improve productivity and increase R&D

spending by companies the Government introduced two credits. In 2000-01 the Government introduced a

scheme for small and medium enterprises (SME) with a separate scheme for large enterprises in

2002-03 to encourage scientific and technological innovation within the United Kingdom. The

conditions defining what activities and expenditures qualify as R&D are generally the same in both

the SME scheme and the large company scheme. However, a large company cannot claim for

sub-contracted R&D costs, but it can claim for contributions to independent research. These credits

were tailored to help reduce the cost of corporate R&D which would encourage more R&D spending by a

company and as a consequence increase the innovation in the economy.

For expenditures

incurred up to and including 31 July 2008, an SME can deduct 150% of their qualifying R&D

expenditure and the payable tax credit 16%. For expenditures incurred on or after 1 August 2008, an

SME can deduct 175% of their qualifying R&D expenditure and the payable tax credit of 14%. The rate

is further increased from 1 April 2011 to 200% and a payable credit of 12.50%. From April 1st, 2015

the SME scheme has increased the credit a company can get to 230% on their qualifying R&D costs with

a payable credit of 14.50%.

Large companies can deduct 130% in respect to qualifying

expenditure incurred after 31 March 2008. Furthermore, a stand-alone payable credit scheme was

created for large companies’ research and development (R&D) expenditure incurred on or after 1 April

2013 known as the Research and Development expenditure credit (RDEC). This is also known as ‘Above

the Line R&D Tax Relief’ since the payable credit for large companies is shown above the tax line

and can be accounted for as income in a company’s profit and loss statement. The RDEC and the

current large company super deduction scheme will co-exist until 31 March 2016. The existing large

company scheme rules and benefits will remain unchanged until it ceases in April 2016. After April

2016, all claims for R&D undertaken must be made under the RDEC scheme for large companies.

Company Size and Structure

In order to determine if your company falls under the SME we look at;

- The staff headcount is less than 500 or,

- Either the annual turnover is under €100m or the balance sheet total is less than €86m.

Benefit for SMEs

- From April 1st, 2015 the SME scheme has increased the credit a company can get to 230% on their qualifying R&D costs with a payable credit of 14.50%.

Benefits for Large Companies

- Under the Large companies scheme a company can deduct 130% in respect of qualifying expenditure incurred after 31 March 2008.

- From 1 April 2015, the tax relief is given at 11% on the amount of qualifying R&D expenditure under the RDEC scheme.

- Companies with no corporate tax liability can benefit through a cash payment (with limitations) or a reduction of taxes that are due.

Detailed guidance on linked and partner companies can be found at:

Basic Requirements

The basic requirements for research activities to qualify:

- A company must be undertaking a project to seek an advance in science or technology through the resolution of scientific or technological uncertainties.

- The advance being sought must constitute an advance in the overall knowledge or capability in a field of science or technology, not a company’s own state of knowledge or capability alone.

- Qualified research activities are defined as the development or improvement to a business component, which can include creating new processes, products or services, making appreciable improvements to existing ones and even using science and technology to duplicate existing processes, products and services in a new way.

- The research must be technological in nature. That is the process of experimentation used to discover the information fundamentally relies upon the physical or biological sciences, engineering or computer science. Furthermore, companies may use existing technologies and may rely upon existing principles to satisfy this requirement.

- The search must be intended to eliminate uncertainty concerning the development or improvement of a business component. Scientific or technological uncertainty exists when knowledge of whether something is scientifically possible or technologically feasible, or how to achieve it in practice, isn’t readily available or deducible by a competent professional working in the field.

- Elimination of the technical uncertainty must be accomplished through a simulation.

Activities That May Qualify

- Developing new products

- Developing new, improved or more reliable products, processes or formulas

- Developing prototypes or pilot models

- Developing new tools, jigs, molds or dies

- Developing or applying for patents

- Testing new product designs

- Developing new technology

- Developing or improving production or manufacturing processes

- Developing new software applications

- Expending resources on outside consultants or contractors to do any of the above-stated activities.

HMRC R&D Guidelines

For more information on IRS R&E Guidelines, see:

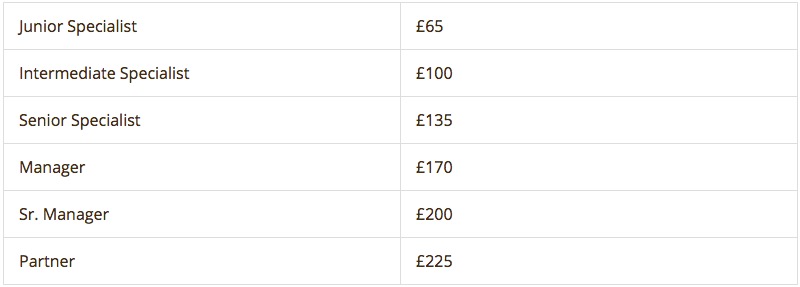

Pricing

Pricing varies by case, please Contact Us to request a quote.

Standard Rates